The $70B Exit: Bitcoin Miners Are Leaving Bitcoin.

Here's who wins:

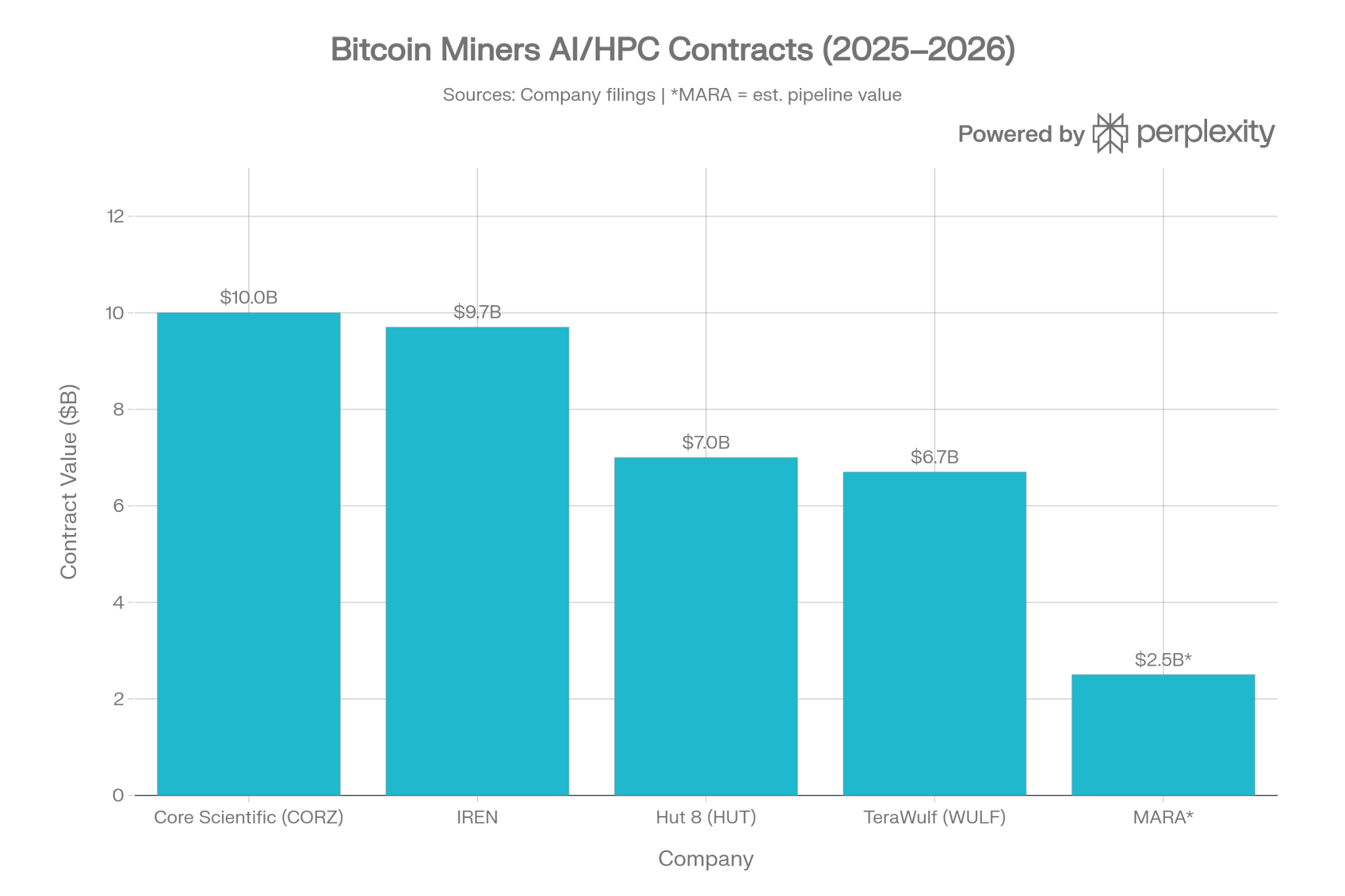

Bitcoin mining companies have signed $70 billion in AI data center contracts.

MARA dumped 15,000 BTC in three weeks.

Bitdeer sold every single coin in its treasury.

Miner debt exploded 500% in a single year.

Iran bombed the world’s biggest LNG plant.

It all means something.

For Bitcoin miners specifically:

Every miner that leaves makes the math better for every miner that stays.

TLDR

Public miners carry $12.7B in debt from a hashrate arms race that overheated the network. The math is broken for most listed miners.

The AI pivot is rational: a 250 MW site is worth 10x more as an AI data center. Listed miners may pull 70% of revenue from AI by December.

The Ras Laffan LNG attack spiked global gas prices 32%, but US Henry Hub stays flat thanks to export terminal bottlenecks. US miners are insulated, for now.

Permian Basin gas prices went negative 38 out of 51 trading days in 2026. Stranded gas miners pay nothing to hash.

The crisis is a sorting mechanism: stranded gas, remote hydro, and low-cost private miners inherit the network.

All of this covered in a 5min read →

Bitcoin mining is not dying, it’s splitting

Public miners could generate 70% of their revenue from AI by December 2026:

That is up from about 30% today.

This is not mere “diversification”, this is a full identity change.

And the backstory matters.

Bitcoin miners entered the 2024 halving carrying $12.7 billion in debt.

That is up from $2.1 billion the year before (500% increase)

VanEck called it the “melting ice cube problem.”

A miner that skips one hardware cycle loses network share forever.

So miners kept borrowing to hold their place in line

The hashrate hit 1.15 ZH/s in October 2025 (+44% in 10 months)

But public miners only contributed about 80 EH/s of that growth.

The rest came from private operators, state-backed miners (Russia & China), and hydro facilities in Ethiopia and Paraguay running at 1-3 cents per kWh.

The key point:

Public miners borrowed at 8-12% interest to compete against operators whose power was essentially a rounding error.

The April 2024 halving cut the block subsidy to 3.125 BTC.

Hashprice dropped 44%, from $50/PH/day to $28/PH/day in February 2026.

The weighted average cost for public miners hit $79,995 per BTC.

The math speaks for itself.

The Great AI Pivot

So the public miners did what any rational economic actor does when the core business bleeds cash.

They pivoted.

The evidence:

MARA sold 15,133 BTC in three weeks ($1.1 billion) to buy back debt.

Bitdeer sold every coin in its treasury and raised $368 million for AI deals

Riot sold $200 million of BTC.

Bitfarms dropped “bitcoin company” from its name.

Core Scientific is directing 1.3 GW of Texas power capacity to AI hosting.

Go to any of these companies’ websites and it’s all AI.

A 250 MW Bitcoin mining facility costs about $250 million to build with uncertain return.

The same 250 MW as an AI data center returns $2.5 billion.

Show me the incentive, and I will show you the outcome.

Miners who hold land and power purchase agreements are sitting on infrastructure that is worth an order of magnitude more to a hyperscaler than to the Bitcoin network.

These companies are not Bitcoin miners anymore.

They are energy infrastructure companies.

Critical detail:

When a mega-miner converts a site to AI, it keeps the land and power contract.

The ASICs get liquidated. S19s and S21s are flooding the secondary market at $15/TH. In 2022, that same hardware traded at $80/TH.

This creates a cascade where cheap machines need cheap power.

The only places left with cheap power and available land are stranded gas wellheads, remote hydro sites in Ethiopia and Paraguay, and international markets with fast permitting.

The AI pivot takes hashrate offline and repurposes the physical facilities that housed it.

And it sends a wave of cheap hardware to the outskirts of the grid.

The LNG Shock Everyone Misread

Now layer in the energy crisis. And pay attention, because the headlines are misleading.

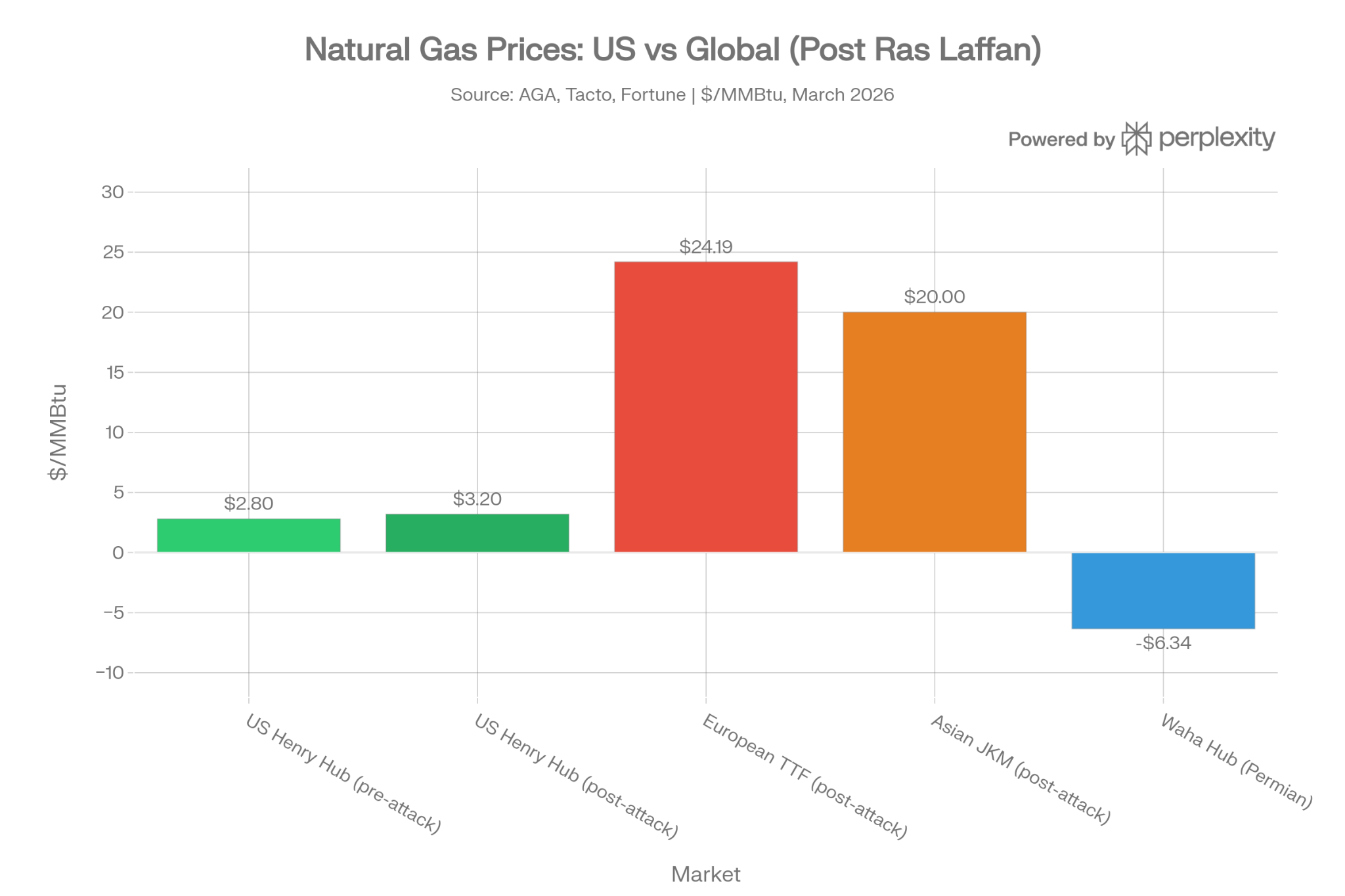

Iran struck Qatar’s Ras Laffan Industrial City on March 18.

This is the world’s largest LNG complex.

Two production trains were damaged and Qatar’s energy minister says repairs take 3 to 5 years (QatarEnergy halted all LNG production)

The Strait of Hormuz closure locked in existing Gulf LNG inventory, cutting about 20% of global LNG flows.

European TTF gas prices surged 32% overnight to $24.19/MMBtu.

Lloyd’s List called it “immediate and immense” with “no spare capacity” in the global LNG market to absorb the loss.

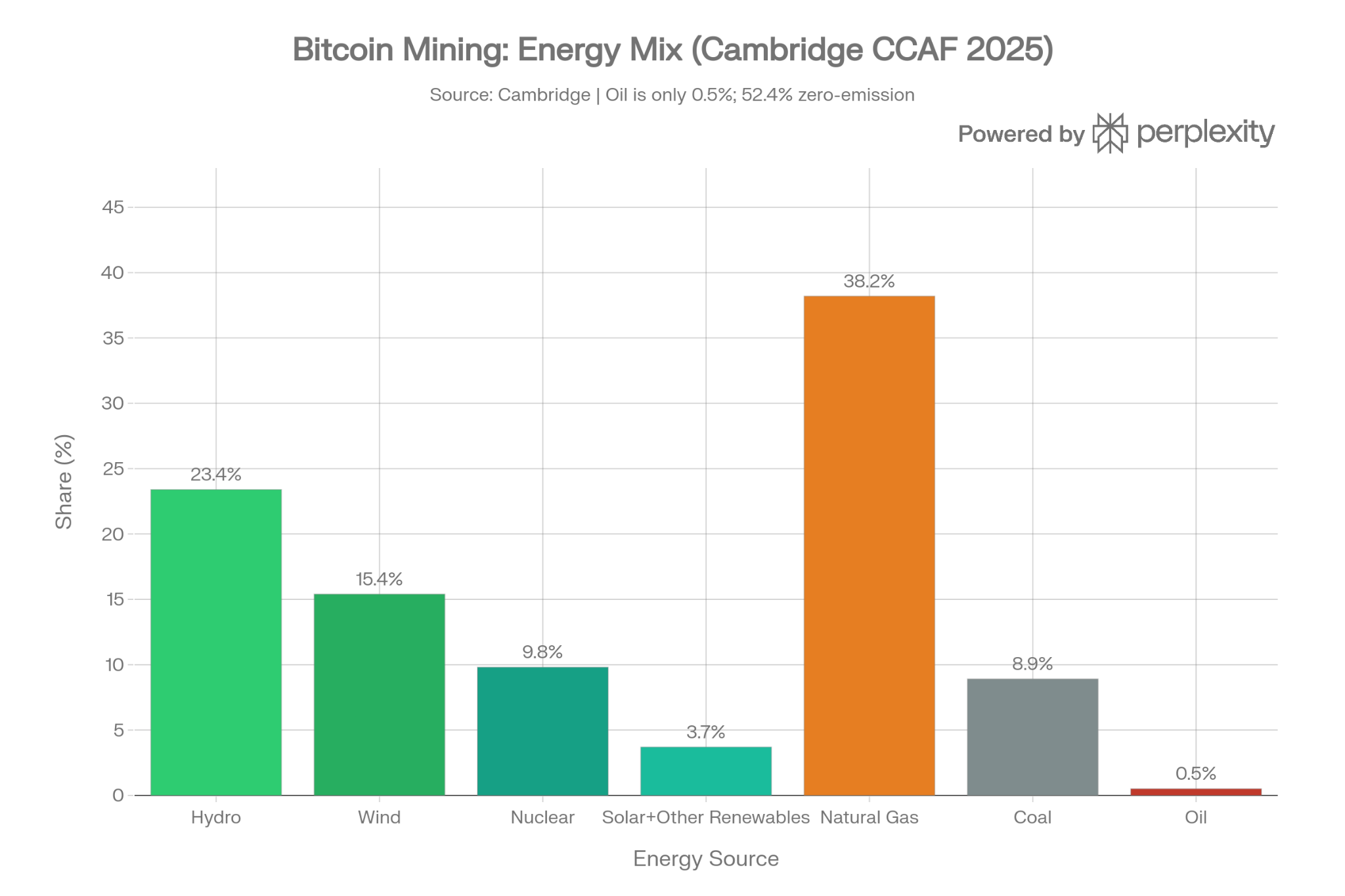

Natural gas represents 38.2% of Bitcoin’s total energy input. It is the single most important fuel for mining. When people say “oil exposure,” they undercount the real risk, which runs through natural gas and US grid prices.

Most analysts concluded: rising energy costs crush Bitcoin miners.

But, US domestic natural gas prices have stayed flat.

Henry Hub trades between $3.10 and $3.40/MMBtu since the war began. The EIA forecasts a 2026 average of $3.80. Why? US LNG export terminals are at full capacity. The gap left by Qatar cannot be filled by US exports. But that also means the global price spike does not drain US domestic supply. Export bottlenecks insulate Henry Hub from TTF and JKM.

For the 90%+ of US mining that runs on grid-supplied natural gas, the Ras Laffan attack is far less damaging than the 2022 European energy crisis was for European miners. The risk scenario exists (Tacto forecasts Henry Hub reaching $5.50 to $8.00 if the Hormuz closure persists), but the base case is stability.

The Permian Basin Paradox

Now here is the part that flips the whole narrative.

The Waha Hub spot natural gas price in West Texas has been negative for 38 out of 51 trading days in 2026. On some days, prices fell to negative $9.75/MMBtu, which means Permian Basin producers are paying to have their gas taken away.

Permian wells produce excess gas as operators drill into gas-rich intervals.

Pipeline capacity to move that gas is 12 to 18 months behind demand.

Record output of 27.6 Bcf/d has nowhere to go.

Blackcomb Pipeline (2.5 Bcf/d) arrives later in 2026.

Until then, the gas is stranded.

For a Bitcoin miner with a container full of the machines they got at a discount from a pubco miner, strategically positioned at the wellhead, this is the inverse of a crisis.

The fuel is free.

On negative-price days, the producer pays the miner to consume the gas.

At that cost structure, any model is profitable.

Crusoe Energy (partnered with ExxonMobil), Giga Energy Solutions, and BigSur Energy already run containerized operations on Permian and Bakken stranded gas. The FLARE Act provides full expensing for this infrastructure. Texas HB 591 adds severance tax exemptions.

So:

The global LNG crisis could make grid electricity more expensive but stranded gas upstream is largely unaffected.

The Sorting Framework

This brings us to the thesis:

the AI pivot and the LNG crisis are not bad for Bitcoin mining across the board.

They’re a sorting mechanism →

Stranded gas miners: Power is effectively zero. Immune to global LNG pricing. This is the natural destination for mining (i.e. Kardashev Type I)

International hydro miners (Ethiopia, Bhutan, Paraguay): Power at 1 to 3 cents per kWh. Insulated from the LNG shock. Receiving cheap liquidated machines from the AI pivot. Profitable and expanding.

US grid-tied miners with next-gen hardware: On-grid US miners with stable power purchase agreements independent of O&G inflation. Difficulty drops help. The 20% cumulative difficulty reduction from February to March 2026 boosted per-hash revenue by about 25%. (Simple Mining falls into this bucket with 65% wind power)

Everyone else: Cash-negative, shutting down, selling hardware, and pivoting to AI if possible.

What To Watch

The difficulty adjustments. The next estimate is +5.32%. If it comes in flat or negative, more miners are leaving.

Waha Hub spot prices. If negative pricing persists through Q2 (and it should, with pipeline capacity months away), stranded gas mining economics stay extraordinary.

Henry Hub vs. TTF spread. As long as US export terminals stay at capacity, the decoupling holds. If new terminal capacity comes online or policy changes allow more exports, the insulation breaks (no incentive to do this)

The 2028 halving shadow. At current economics, a much higher BTC/USD price is needed for the majority of public miners to conduct any mining business. Only miners building sub-4 cent infrastructure now will be viable at any Bitcoin price below $120K after the next halving.

The network does not care who leaves. It reprices the reward for those who remain.

Should be another interesting week in markets.

Where the energy flows, the money follows.

References:

Debt among Bitcoin miners has ballooned from $2.1 billion to $12.7 billion in just one year

70% of “miner revenue” will come from AI by the end of 2026.

Public miners added 80 EH/s in 2025

LNG supply disruption will be ‘immediate and immense’

- Billy Boone

$70B pivoting to AI/HPC is a huge structural shift. Mining hardware and the energy infrastructure behind it translates well to high-density compute workloads, so the pivot makes operational sense. The interesting downstream question is whether miners who fully exit Bitcoin weaken the network's hashrate security, or whether new entrants absorb that capacity quickly enough that it's a non-issue.