Why America Mines 38% of Bitcoin on Borrowed Silicon

and what it means for your mining portfolio

The United States currently mines 38% of the world’s Bitcoin (estimated based on mining pool data, ASIC trading flows, and firmware adoption)

This equates to somewhere in the ballpark of 350 Exahash

But every machine behind the hash is hardware from three Chinese companies, and every chip inside those machines comes from one Taiwanese foundry.

The two American companies that almost broke that dependency both quit in the last 90 days.

TLDR

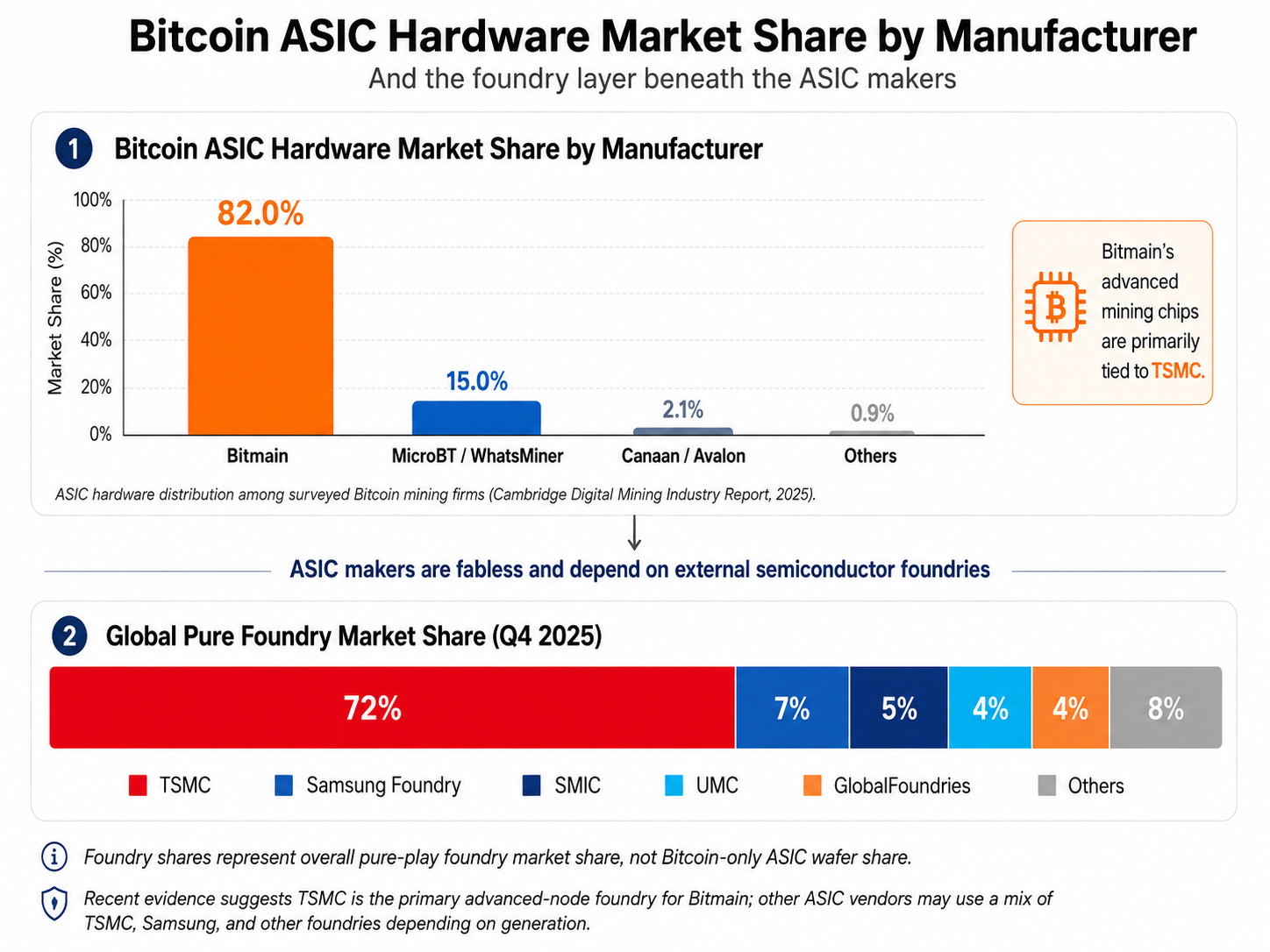

Bitmain accounts for ~82% of deployed ASIC hardware among surveyed miners, MicroBT ~15%, Canaan ~2%, and others <1%.

TSMC makes nearly every Bitcoin mining chip and AI is eating their wafer allocation. Apple alone locked over 50% of the 2nm node.

Velaura AI (Formerly Auradine), the best-funded US challenger ($153M raised), pivoted to AI chips in March. Block’s Proto status is uncertain after Dorsey cut 40% of staff in February.

S23 series pricing has already slipped to about $22/TH. Hashprice sits at $27.70 per PH/s/day. The squeeze is structural.

The Mined in America Act exists, but there is no fab

The Question No One in DC Wants to Answer

If China decides tomorrow that Bitcoin mining hardware is a strategic export (like rare earths), what happens to America’s 38% share of hashrate?

Right now nobody has a real answer.

There’s no domestic fab and there’s barely a domestic chip designer.

The Concentration Problem

The University of Cambridge study published in April 2025 puts Bitmain at 82% of global ASIC production, MicroBT at 15%, and Canaan at roughly 2%.

This is the most concentrated bottleneck in Bitcoin.

This is due to 13 years of compounding chip design experience at the same fab. Nobody else is even close.

The Real Bottleneck Sits in Taiwan

Most people think Bitmain is the choke point. The actual choke point sits one layer deeper.

TSMC holds 71% of the global foundry market. Samsung, the nearest competitor, holds 6.8%.

Every meaningful efficiency gain in mining since the S9 came from TSMC moving down a node.

TSMC’s 3nm capacity is running at 100% utilization right now.

NVIDIA’s Rubin GPU is on 3nm. AMD’s MI355 series is on 3nm.

NVIDIA alone has booked over half of TSMC’s CoWoS advanced packaging.

The 2nm node is gone before Bitmain gets a bid.

Apple locked up over 50% of the initial allocation for the iPhone 17 and the M6 Mac. AMD’s Zen 6 took most of what was left.

Bitcoin mining isn’t even in the conversation at 2nm.

“Show me the incentive, and I will show you the outcome.”

TSMC’s AI revenue was 61% of total revenue in Q1 2026, growing at a 60% CAGR through 2029. Every quarter, the pull toward AI customers gets stronger and absorbs even higher wafer allocation

Reshoring Options

Auradine (now Velaura AI) raised over $153 million, had MARA backing, and was approaching 9.8 J/TH with the Teraflux series.

In March they pivoted to AI chips.

The remaining mining inventory is being used to self-mine.

Block Proto also looked promising.

modular hashboards and open-source fleet management, with the air-cooled rig hitting 819 TH/s at 14.1 J/TH, with more power in the same footprint than Bitmain

Proto designs the Bitcoin mining ASIC in-house at Block, but the wafers are fabricated by an unnamed “leading global semiconductor foundry”

In February, Jack Dorsey cut over 4,000 employees, 40% of Block. He cited AI as the reason.

Nobody outside Block knows whether Proto survives intact as a real product line, especially with hashprice at all time lows and weak air-cooled ASIC demand

So the two best-positioned American challengers have been disrupted by AI to some extent.

The reality is this:

Bitcoin is cyclically deprioritized because AI is now the higher-immediacy, higher-productivity, higher-cash-flow narrative competing for capital, talent, energy, attention, and leverage.

The S23

S23 Air launched at $7,900-$8,000. Hong Kong resellers are already cutting to $7,180 about $22.58 per TH.

S23 Hyd 580T sits at $14,790-$17,400. The 1,160T units run $29,800-$34,800.

Meanwhile, S19 and S21 hardware has collapsed to $3-$7 per TH on secondary markets. What was cutting edge hardware 2 years ago is now a glorified paper weight.

Hashprice is near all time lows:

At these economics, a miner either needs sub $0.05/kWh power, or sub 13 W/TH efficiency

This is Bitmain’s dilemma. If they hold pricing, inventory turnover validates the distressed narrative while TSMC is raising wafer costs 3-5%.

If they cut pricing, it further validates the distress, and in many cases there is no place for the air-cooled models to go with gigawatts of mining infrastructure switching to GPUs.

There’s no easy exit until hashprice moves materially higher.

and price may not improve until Q4 2026.

Difficulty needs to drop 30% from current levels to incentivize ASIC demand.

Then the Tariffs Hit

Trump signed Section 232 tariffs on steel, aluminum, and copper on April 2nd 2026. The classification swept ASIC miners in as “derivative products” with substantial metal content.

The result: a 25% tariff stacked on the existing 21.6% Southeast Asia ASIC import duty.

US miners could pay roughly 47% more for new hardware than competitors in Kazakhstan, Russia, or any tariff-exempt jurisdiction.

So Bitmain opened a US assembly line in January. MicroBT has had one since 2023.

They reduce the tariff burden but don’t eliminate it, because aluminum and copper inputs still get taxed.

Chinese hardware companies are building factories in America to dodge American tariffs on Chinese hardware (effective reshoring if you ask me)

The Mined in America Act

Senators Cassidy and Lummis introduced the bill on March 26.

It creates a voluntary certification, phases out adversary-linked ASICs by 2030, codifies the Strategic Bitcoin Reserve, and lets certified miners sell BTC directly to Treasury at market prices with a capital gains exemption.

The bill instructs NIST to support domestic mining hardware development.

But it doesn’t fund a fab or guarantee wafer allocation.

and the two American companies positioned to actually answer the bill’s call are getting sucked in the AI blackhole.

What This Means For You

Four takeaways, in priority order.

S23 pricing likely isn’t at the floor. Until difficulty or price improves, Bitmain has to cut to move inventory. Patience is a position.

Particularly related to Simple Mining, inventory includes S21 XP air-cooled (270 TH) and S21j XP Hydro (495 TH). The S21j XP inventory is dwindling, and orders have been delayed. So turnkey hydro availability could get pushed to July/August. My guess is Bitmain is trying to work through air-cooled inventory (which demand is plummeting for) before processing hydro orders.

Bitdeer (BTDR) is the only public name with a real shot at displacing Bitmain inside the decade. Jihan Wu’s company runs 63.2 EH/s of self-mining on their own SEALMINER chips. Still TSMC-fabbed and Singapore-headquartered, so this isn’t a US sovereignty alternative.

The “Mined in America” thesis is a 10 year story, not a 2026 trade. Anyone selling you US-sovereign mining is marketing. There is little chip independence, and what capacity is available is going to GPUs

Zoom out and this is the regime: over-specialization is risky and supply chains need backup plans. Prefer assets with low reliance on political promises. Bitcoin the asset passes that test. Bitcoin’s hardware supply chain not so much.

The Numbers to Watch

TSMC’s AI/HPC revenue mix. It was 61% of revenue in Q126. The higher it goes, the lower ASIC makers drop down priority list at every node review. This will be what moves difficulty. It is the only hope for hashprice recovery.

the AI chip complex itself. Leopold Aschenbrenner’s fund holds $8.5 billion in puts on NVDA 0.00%↑ , TSM 0.00%↑ C, and SMH 0.00%↑.

If he’s right and chips reprice, wafer allocation frees up, ASIC prices fall, and mining hardware economics improve from the supply side.

The semiconductor sector is priced for perfection: SOXX trades around 82x earnings after roughly doubling YTD, while tech’s share of the S&P 500 has exceeded the dot-com peak.

If the AI chip complex cools, capital may rotate from earnings-based digital infrastructure into protocol-based scarcity.

That would make Bitcoin the deep value “scarce digital asset” trade left standing.

For miners, the best-case outcome is even more interesting: semi weakness could loosen wafer allocation and push ASIC prices lower, improving mining economics from the supply side (if BTC/hashprice holds up)

- Billy